A significant shift is underway in the global financial landscape. China is accelerating its long-standing campaign to reduce the world’s reliance on the US dollar, a process known as de-dollarization. This strategic push involves promoting its own currency, the renminbi (RMB), for international trade and investment. This article explores the key drivers behind China’s de-dollarization efforts, the surge in overseas renminbi lending, and the implications for the future of the global monetary system.

The Surge in Renminbi Lending

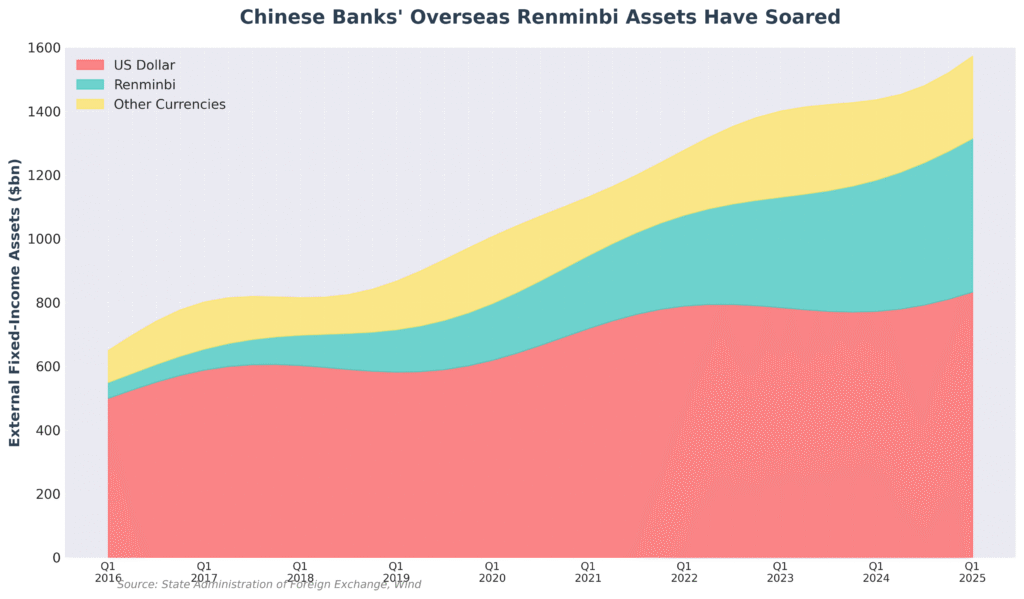

Recent data reveals a dramatic increase in China’s overseas lending in its own currency. Chinese banks’ external renminbi loans, deposits, and bond investments have quadrupled to over Rmb 3.4 trillion ($480 billion) in the last five years. This surge is a clear indication of Beijing’s commitment to establishing the renminbi as a major international currency.

Source: State Administration of Foreign Exchange, Wind [1]

As the chart above illustrates, the growth in renminbi-denominated assets has been substantial, particularly in comparison to the relatively stable holdings of US dollar assets. This trend is further corroborated by the Bank for International Settlements (BIS), which notes a significant pivot towards renminbi-denominated credit for developing countries since 2022.

A Strategic Move Away from the Dollar

China’s de-dollarization strategy is not merely an economic aspiration; it is a defensive measure against the “weaponization” of the US dollar. The use of financial sanctions by the US and its allies has highlighted the risks of over-reliance on a single currency. By promoting the renminbi, China aims to create a more resilient and multipolar global financial system, one less susceptible to the political and economic pressures of any single nation.

“From China’s perspective, [settlement in renminbi] is important because it shows that no matter what happens, it can still trade,” said Adam Wolfe, emerging markets economist at Absolute Strategy Research in London. [1]

The Renminbi's Growing Role in Trade

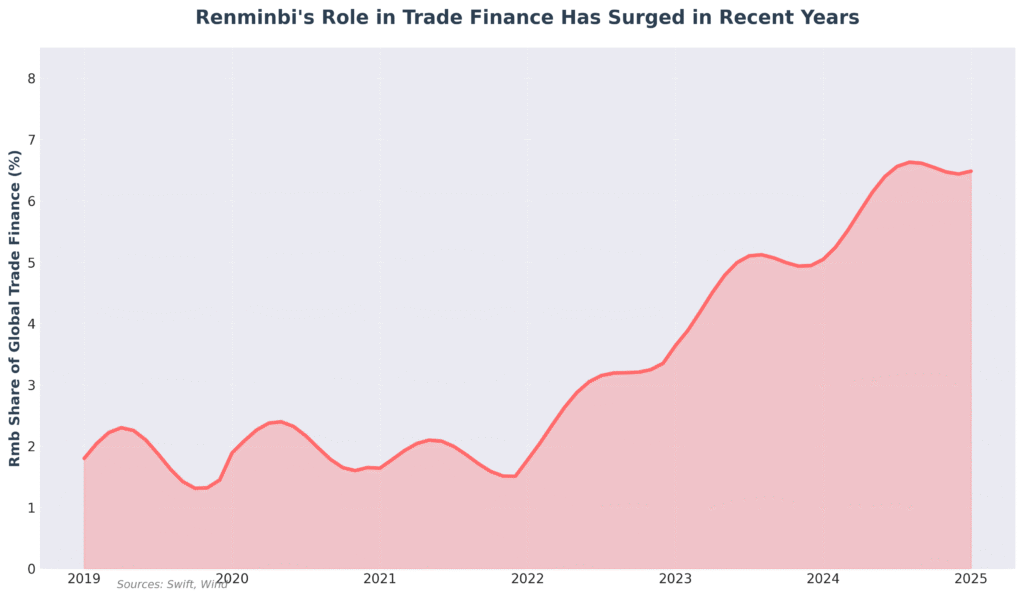

The most significant progress in the internationalization of the renminbi has been in the realm of trade finance. The renminbi’s share of global trade finance has quadrupled in the past three years, reaching 7.6% in September 2025, making it the second most-used currency after the US dollar.

Source: Swift, Wind [1]

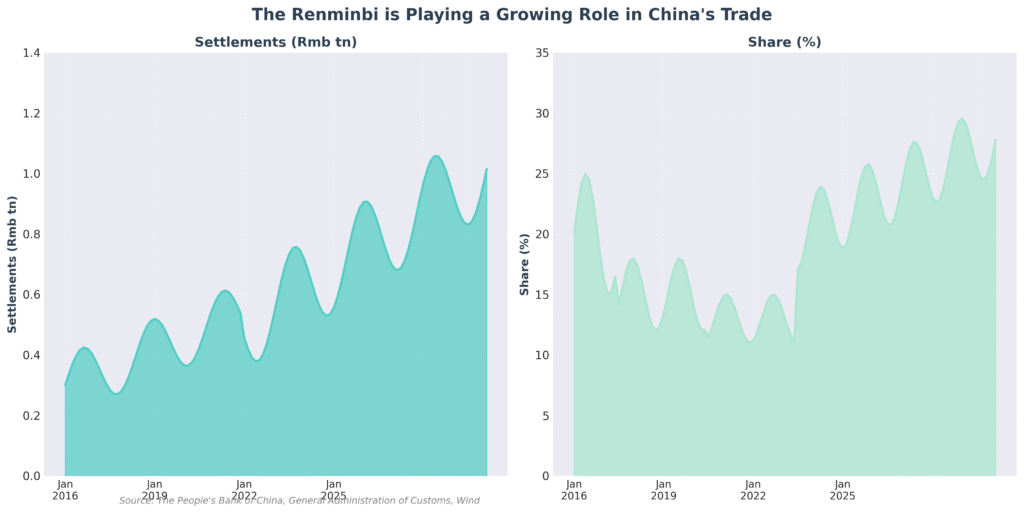

This growth is also reflected in China’s own trade data. Renminbi settlements in China’s goods trade have soared to over Rmb1 trillion a month, with approximately 30% of China’s trade and over half of its cross-border transactions now settled in its own currency.

Source: The People’s Bank of China, General Administration of Customs, Wind, FT calculations [1]

Building a New Financial Infrastructure

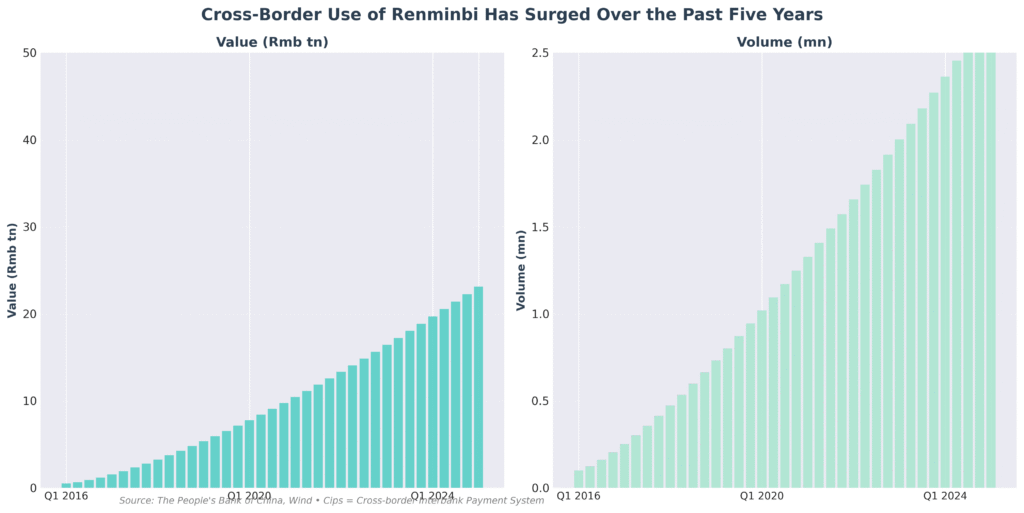

To support the renminbi’s global expansion, China has been actively developing its own financial infrastructure. This includes a network of offshore clearing banks and the Cross-border Interbank Payment System (CIPS). The value of transactions on CIPS has grown exponentially, from a negligible amount a decade ago to over Rmb40 trillion per quarter since the beginning of last year.

Source: The People’s Bank of China, Wind [1]

The rise of CIPS is particularly noteworthy as it provides an alternative to the SWIFT messaging system, which has been central to the US-dollar-dominated financial system.

Challenges and the Road Ahead

Despite these advancements, the renminbi’s journey to becoming a truly global currency faces significant hurdles. Capital controls remain a major obstacle, limiting the currency’s appeal for international investors. As of the beginning of this year, the renminbi accounted for just 2.1% of official global reserves, according to the IMF. [1]

To address this, Chinese policymakers are taking steps to open up their domestic financial markets. Initiatives like the expansion of the Bond Connect program and the opening of the interbank repo market are designed to increase the availability of renminbi-denominated assets and enhance their liquidity.

Conclusion: A Multipolar Future

China’s de-dollarization campaign is a multifaceted strategy with far-reaching implications. While the renminbi is unlikely to replace the US dollar as the world’s primary reserve currency in the near future, its growing role in international trade and finance is undeniable. By building a parallel financial infrastructure and promoting the use of its own currency, China is not just challenging the dominance of the dollar; it is actively shaping a more multipolar global monetary system.

As Bert Hofman, a professor at the National University of Singapore’s East Asian Institute, aptly puts it:

“The policy is moving very gradually, but all of the elements that would make a much more rapid internationalisation work — they’re falling into place.” [1]

The world is witnessing a gradual but steady shift in the balance of global financial power. The rise of the renminbi is a key chapter in this evolving story, one that will continue to shape the future of the global economy for years to come.

References

[1] Sandlund, W., & Ko, H. (2025, October 24). Overseas renminbi lending surges as China steps up campaign to de-dollarise. Financial Times. Retrieved from https://www.ft.com/content/4577100f-8b71-4647-8e7e-fead115d9552